The monetary program (the detour)

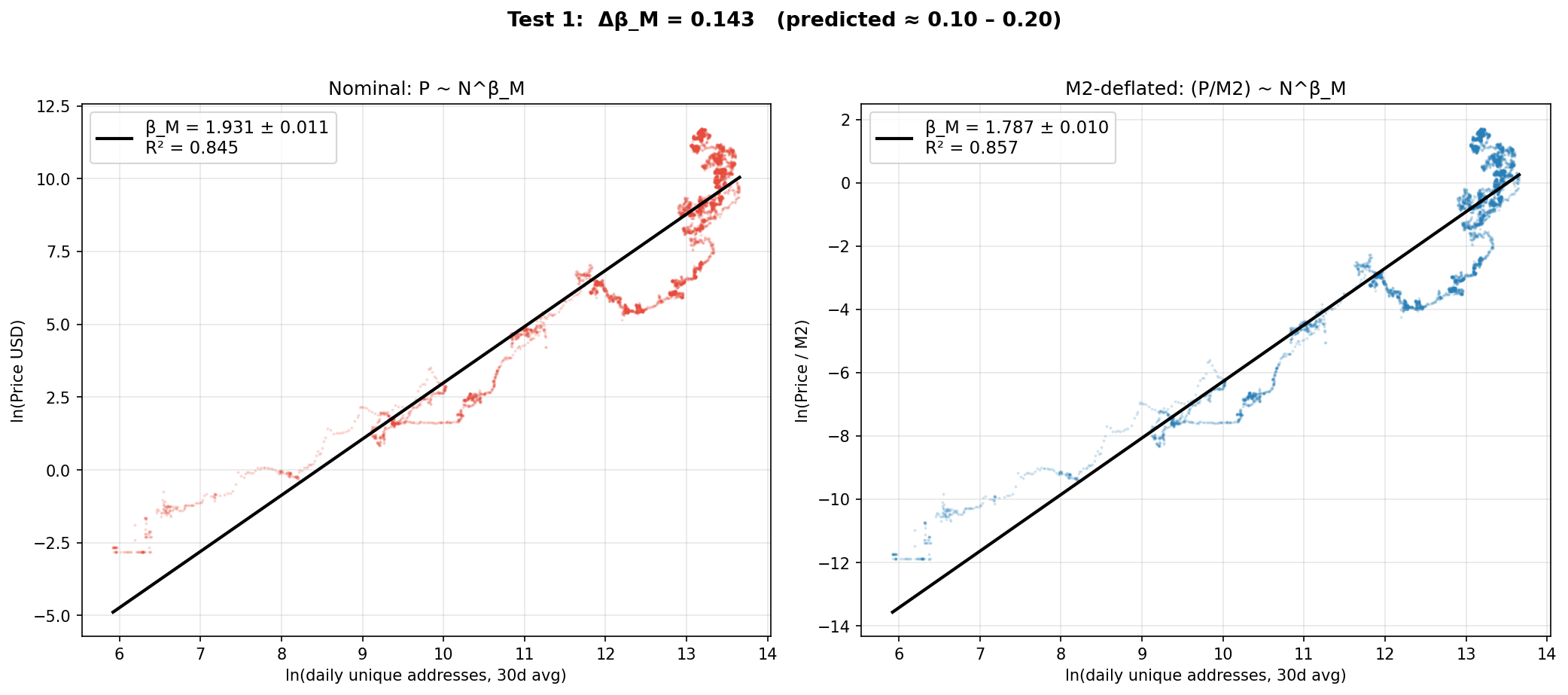

Test 1 detour

M2 deflation

Does deflating by US M2 lower the exponent as predicted?

verdict: supported · results

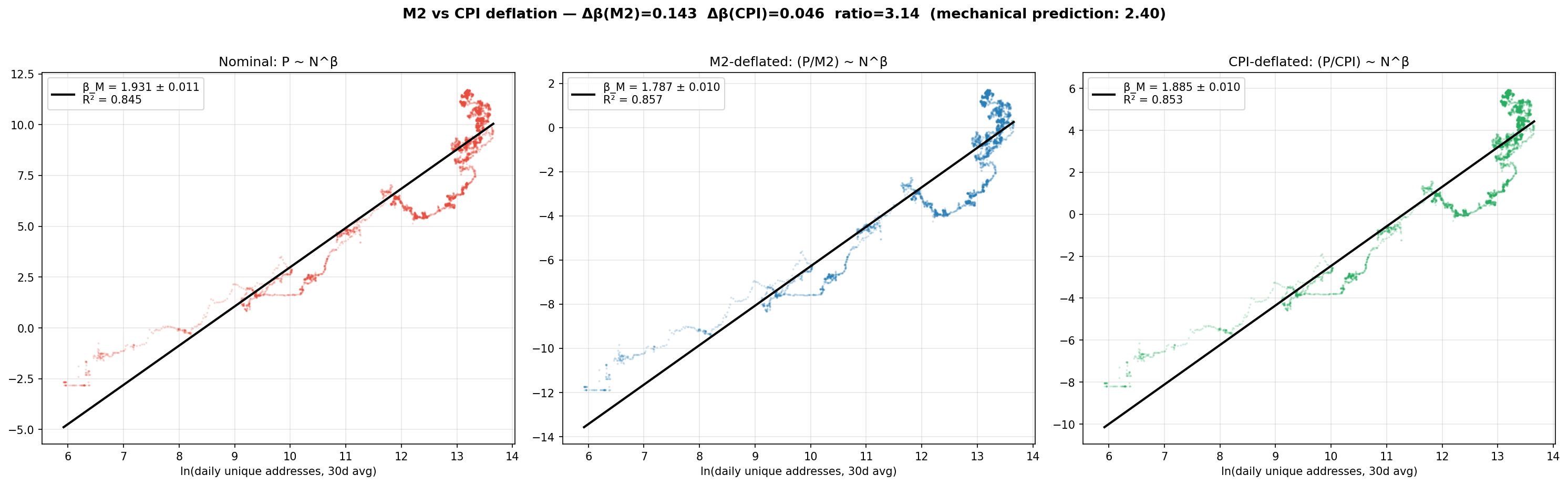

Test 2 detour

M2 vs CPI

Money creation, not price inflation: ratio 3.14 vs 2.40 mechanical.

verdict: supported · results

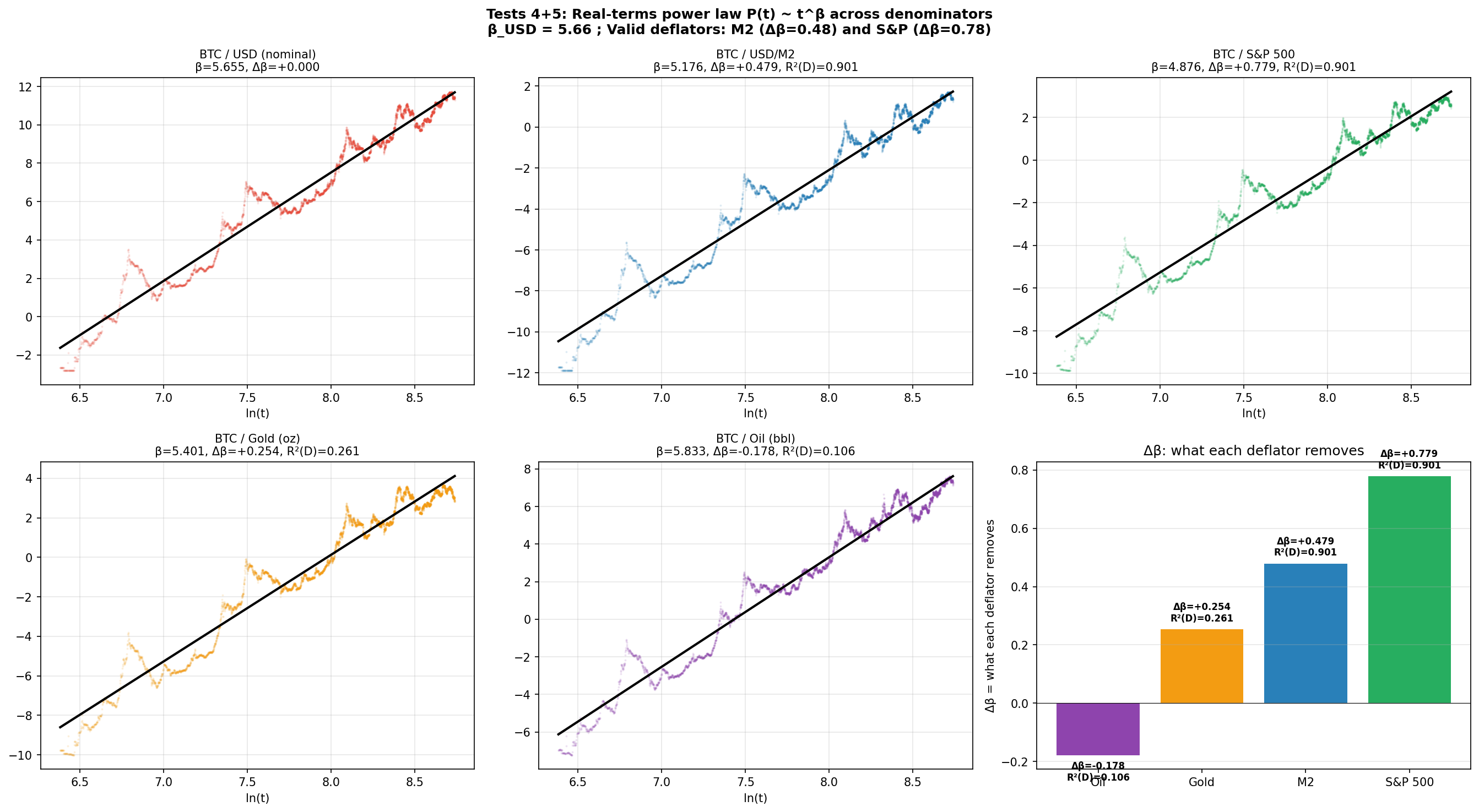

Test 4-5 detour

Deflator hierarchy

M2 and S&P are valid deflators; gold and oil are not.

verdict: supported · results

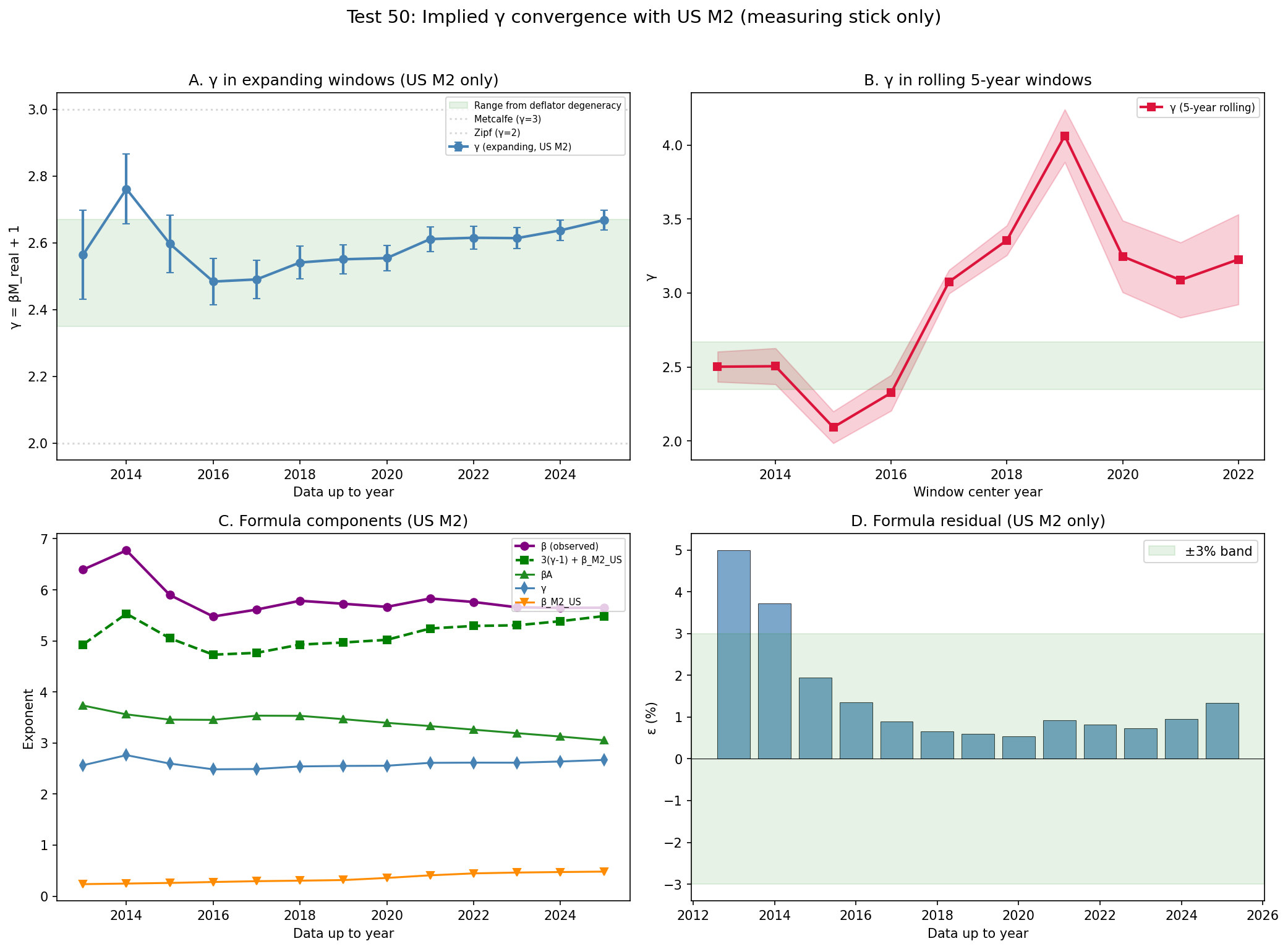

Test 6 detour

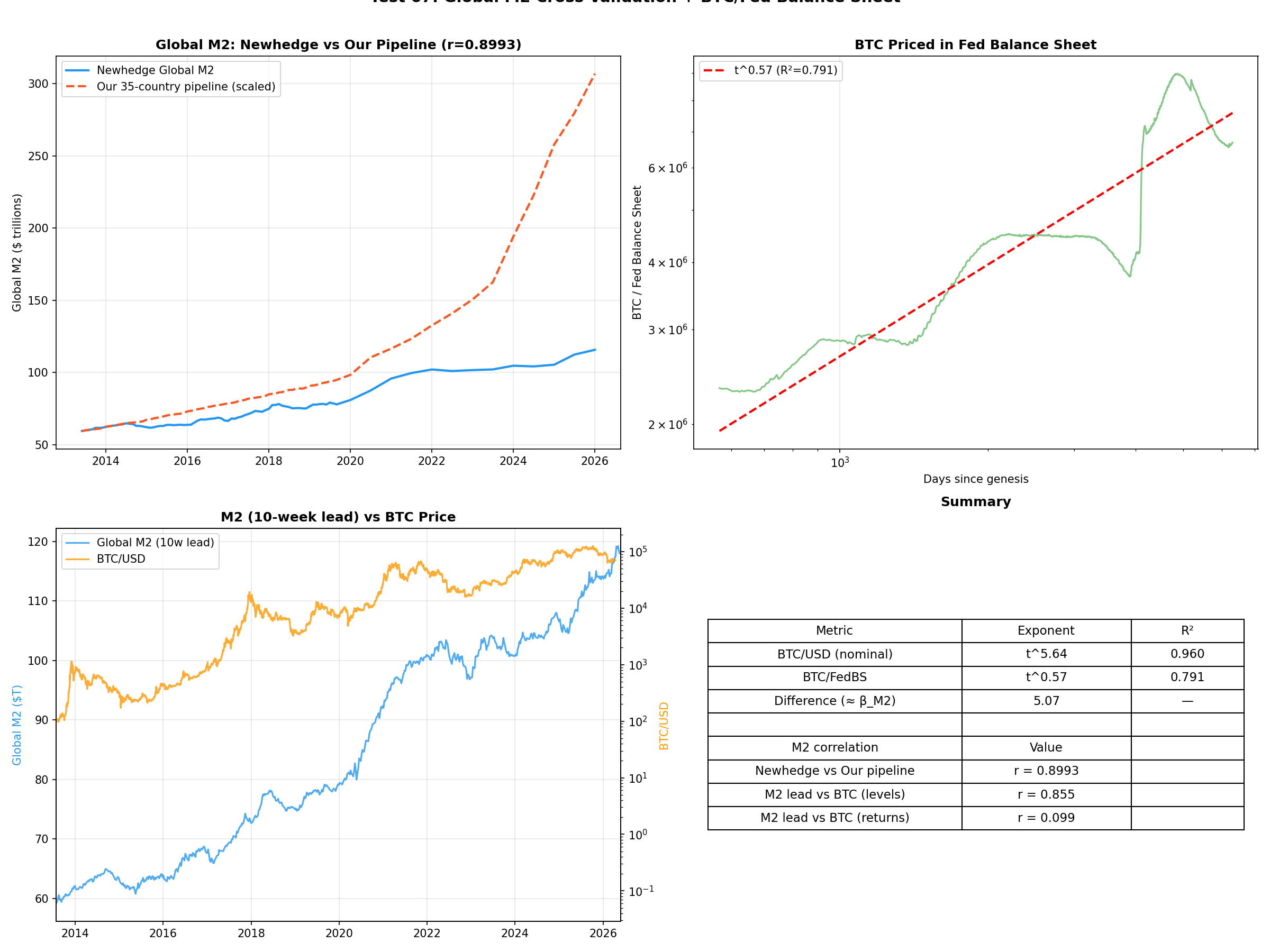

Global M2

A global M2 index removes 22-24% more exponent than US M2.

verdict: supported · results

Test 8 detour

China weight sweep

The global-M2 result holds for any China weight 5-42.5%.

verdict: mixed · results

Test 9 detour

MSCI World deflator

Global equities are not a better deflator than the S&P 500.

verdict: refuted · results

Test 10 detour

Rolling M2 ratio

The global/US ratio is unstable in rolling windows.

verdict: inconclusive · results

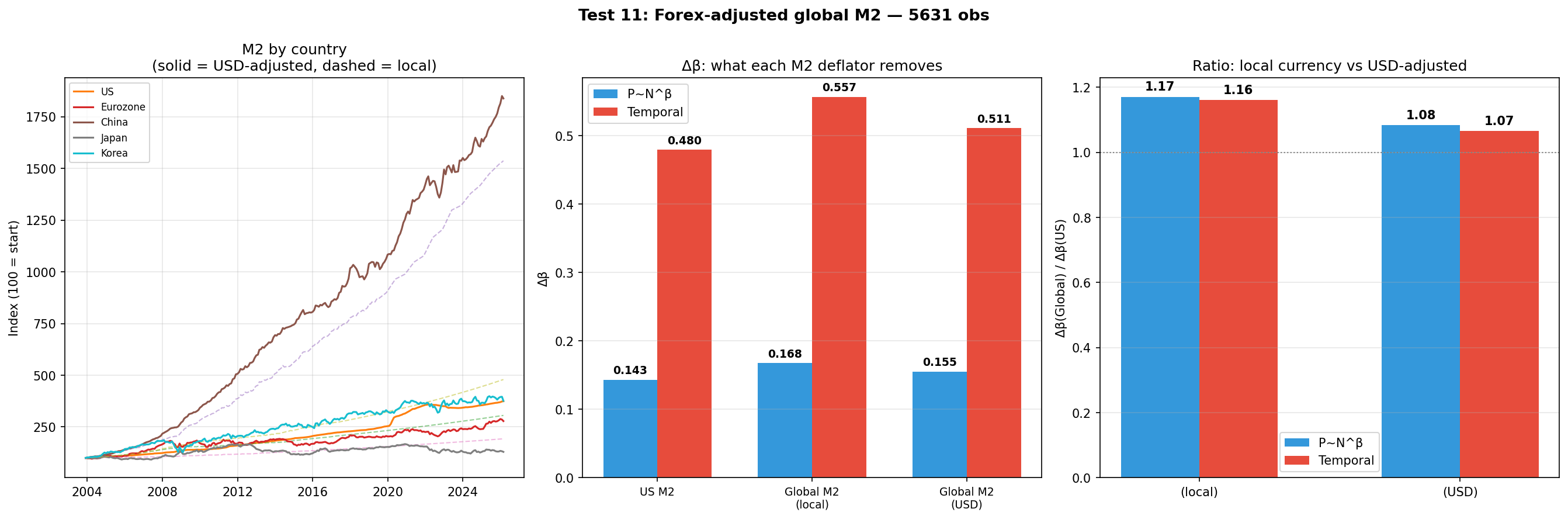

Test 11 detour

Forex-adjusted M2

The global-M2 advantage survives USD conversion (1.08-1.17).

verdict: supported · results

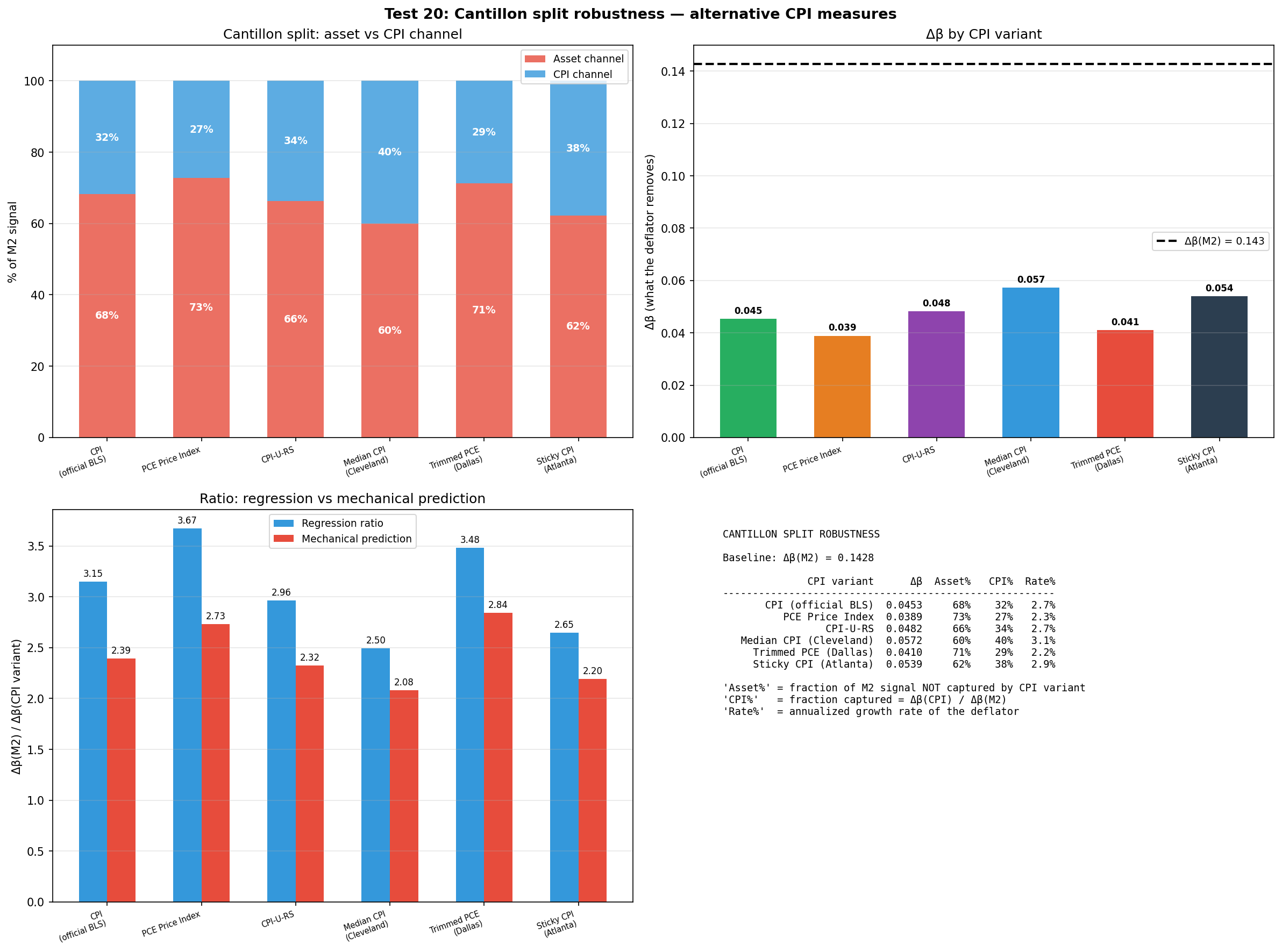

Test 20 detour

Alt-CPI Cantillon

The ~2/3 asset channel survives 6 CPI methodologies (67% +/- 5%).

verdict: supported · results

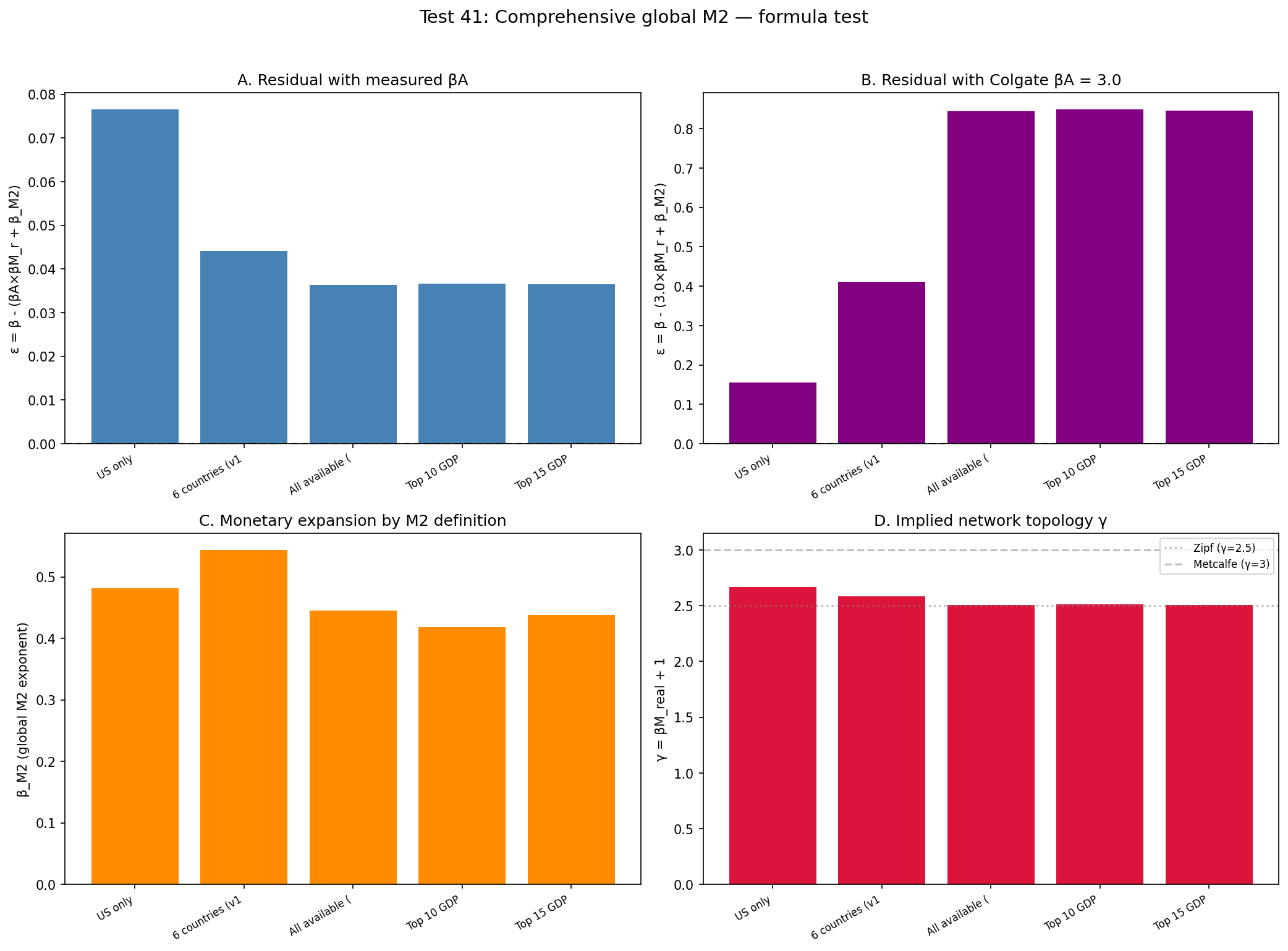

Test 40-43 detour

Global M2 pipeline

17-35 countries: epsilon(Colgate) improves to 2.7%.

verdict: supported · results

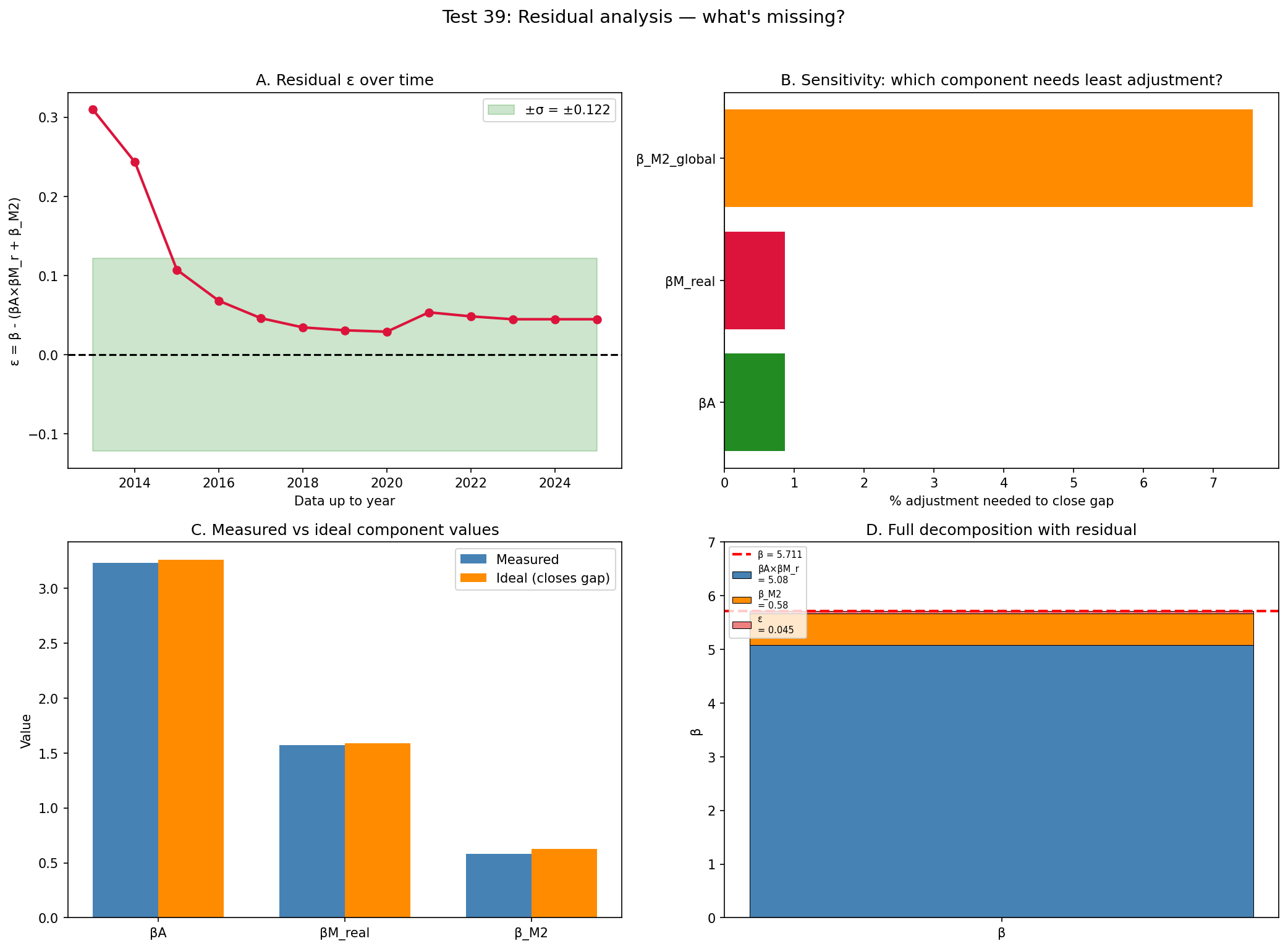

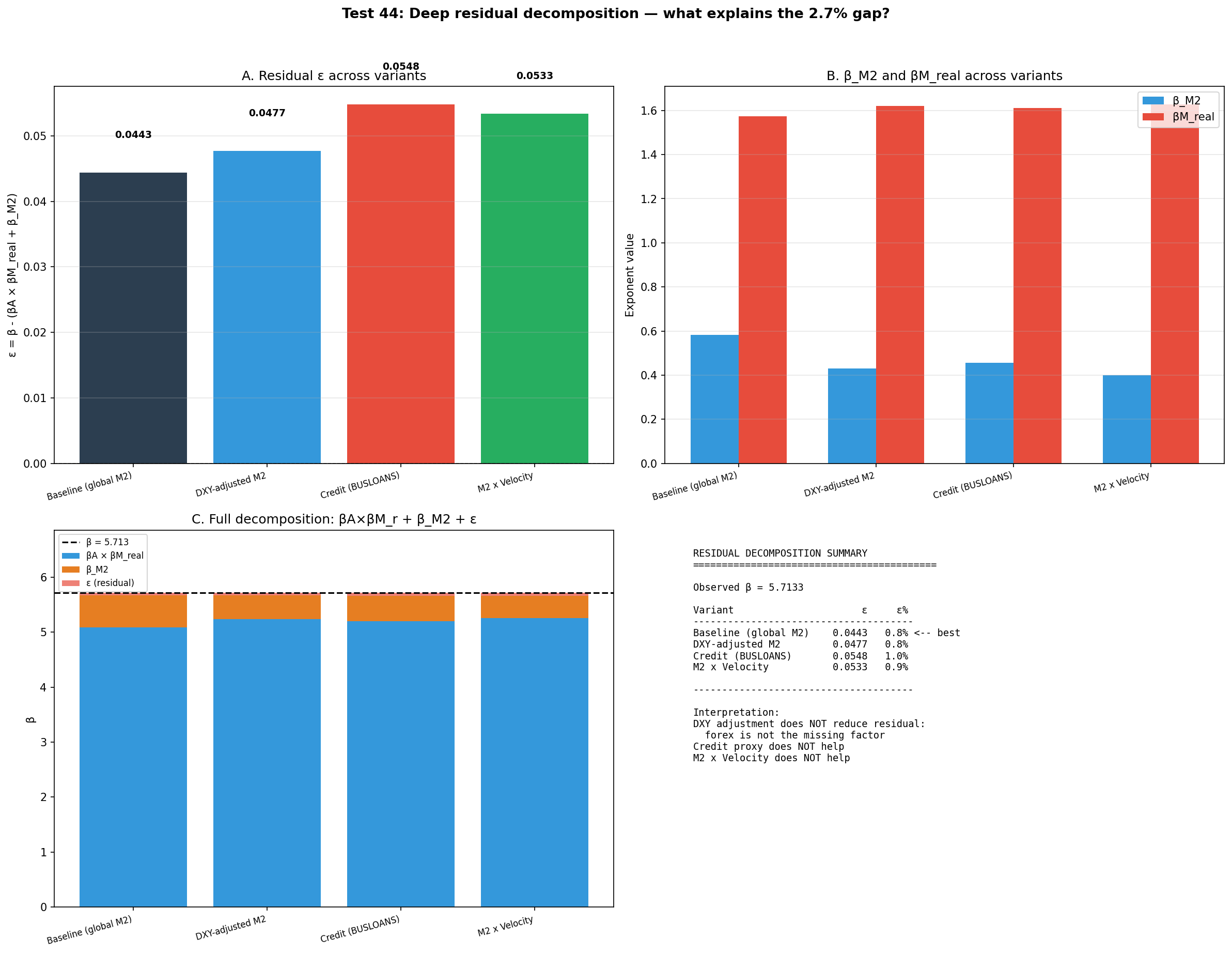

Test 44 detour

Deep residual

No variant (DXY, credit, velocity) beats raw global M2.

verdict: refuted · results

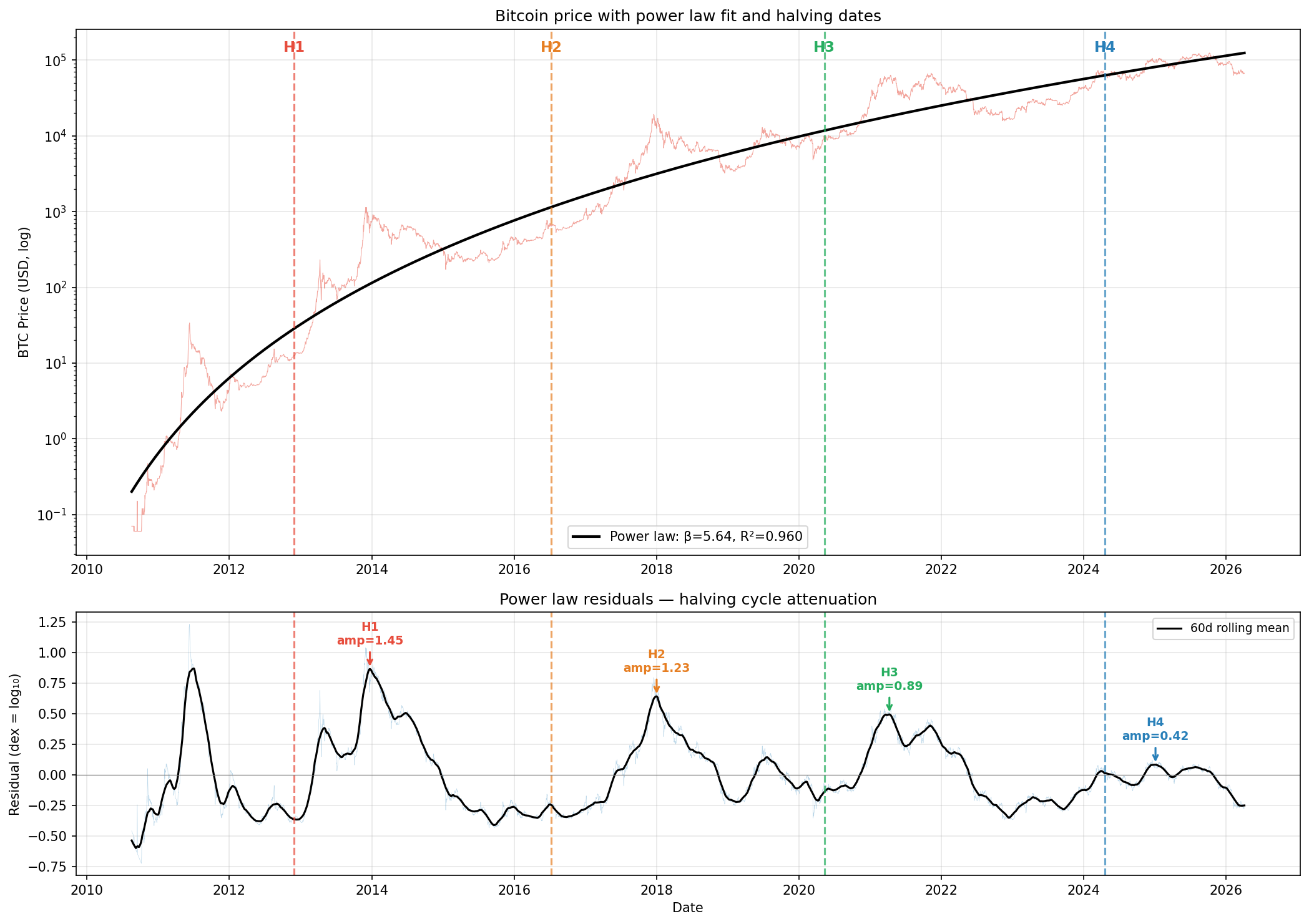

documentary — no figure

Test 46 detour

Two-channel M2

Non-US M2 acts through adoption, not the denominator.

verdict: supported · results

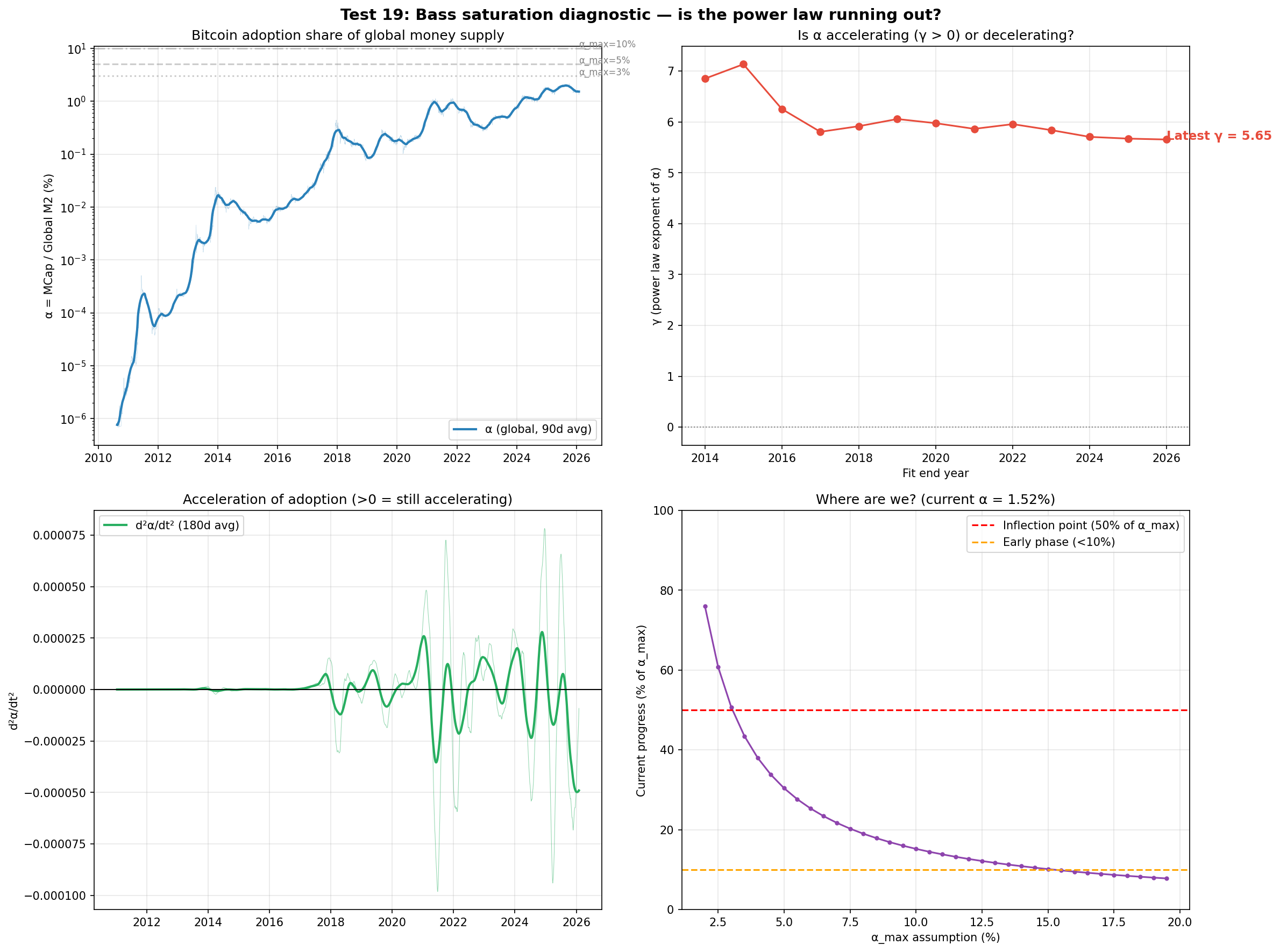

documentary — no figure

Test 47 detour

Deflator comparison

M2 x Loans is the optimal deflator (epsilon = 0.07%).

verdict: supported · results

documentary — no figure

Test 48 detour

Global Cantillon

Globally the split is 49/51, not 68/32 - the US result was local.

verdict: refuted · results

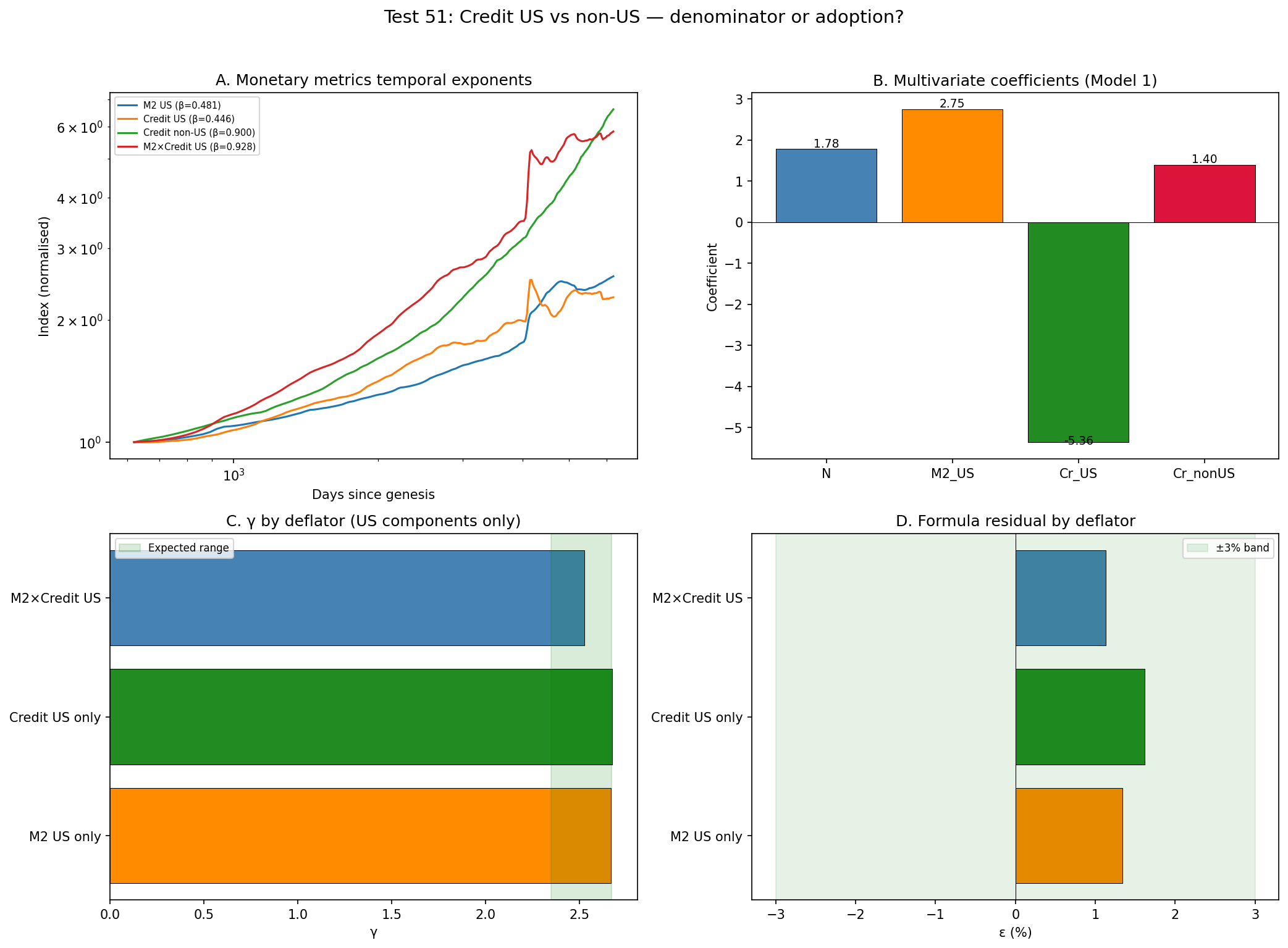

Test 51 detour

Credit US/non-US

Multicollinearity prevents separating the credit channels.

verdict: mixed · results

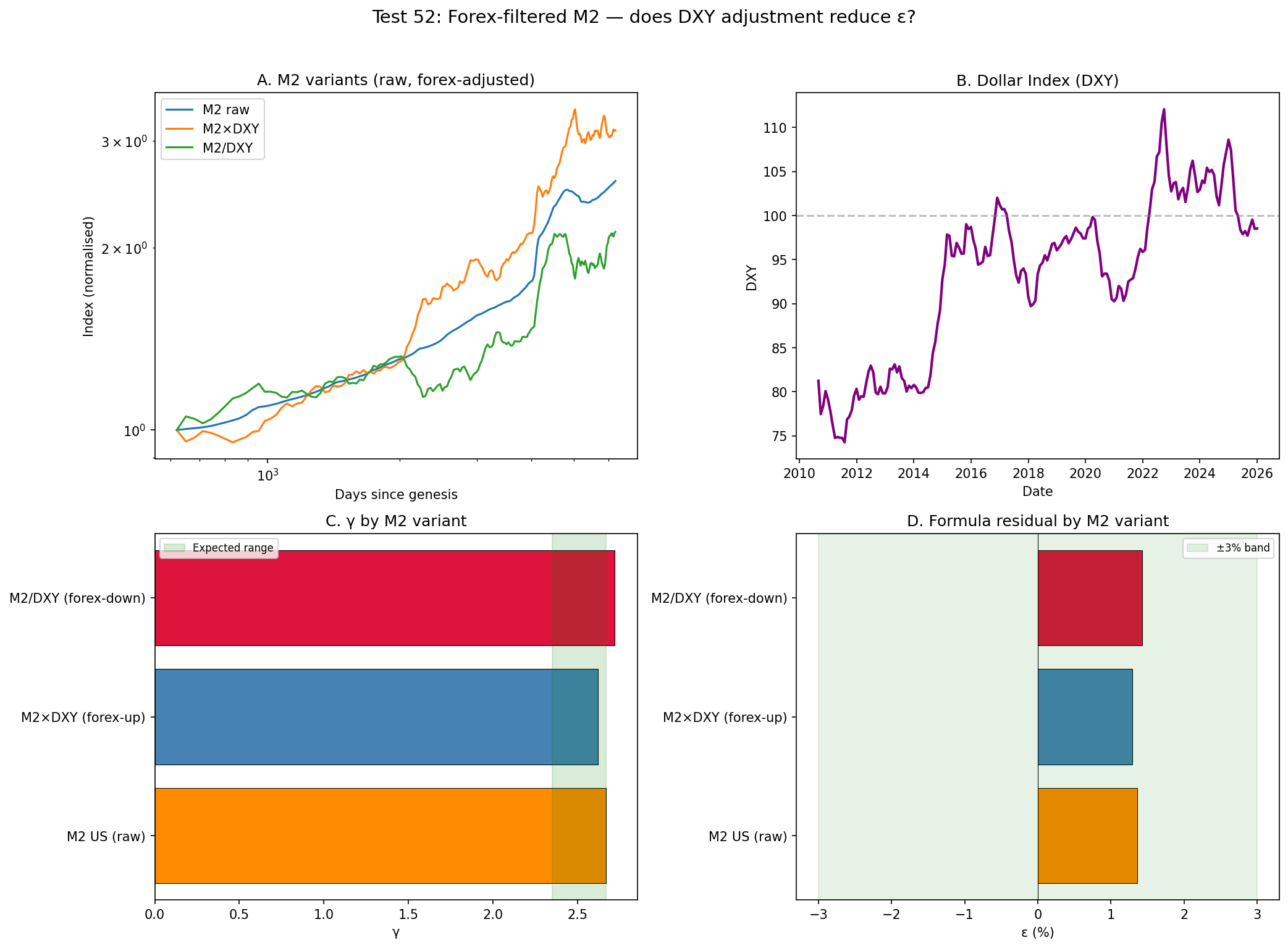

Test 52 detour

Forex residual

DXY adjustment does not reduce the residual (1.4% to 1.3%).

verdict: refuted · results